Every taxpayer takes care of accuracy when filing their Income Tax Returns (ITR). However, mistakes can occur—maybe a deduction was missed, income was reported incorrectly, or an exemption left unnoticed. We all are humans and making such kinds of errors and recognising that errors are a part of human nature.

Keeping such mistakes in mind, The Income Tax Department of India has introduced a provision for filing an Updated Income Tax Return (ITR-U). ITR-U allows taxpayers to correct their submissions post the deadline.

This blog aims to explain what ITR-U is, who can file it, and how it can be utilised to revise previously filed returns.

Contents

Understanding ITR-U/Updated ITR

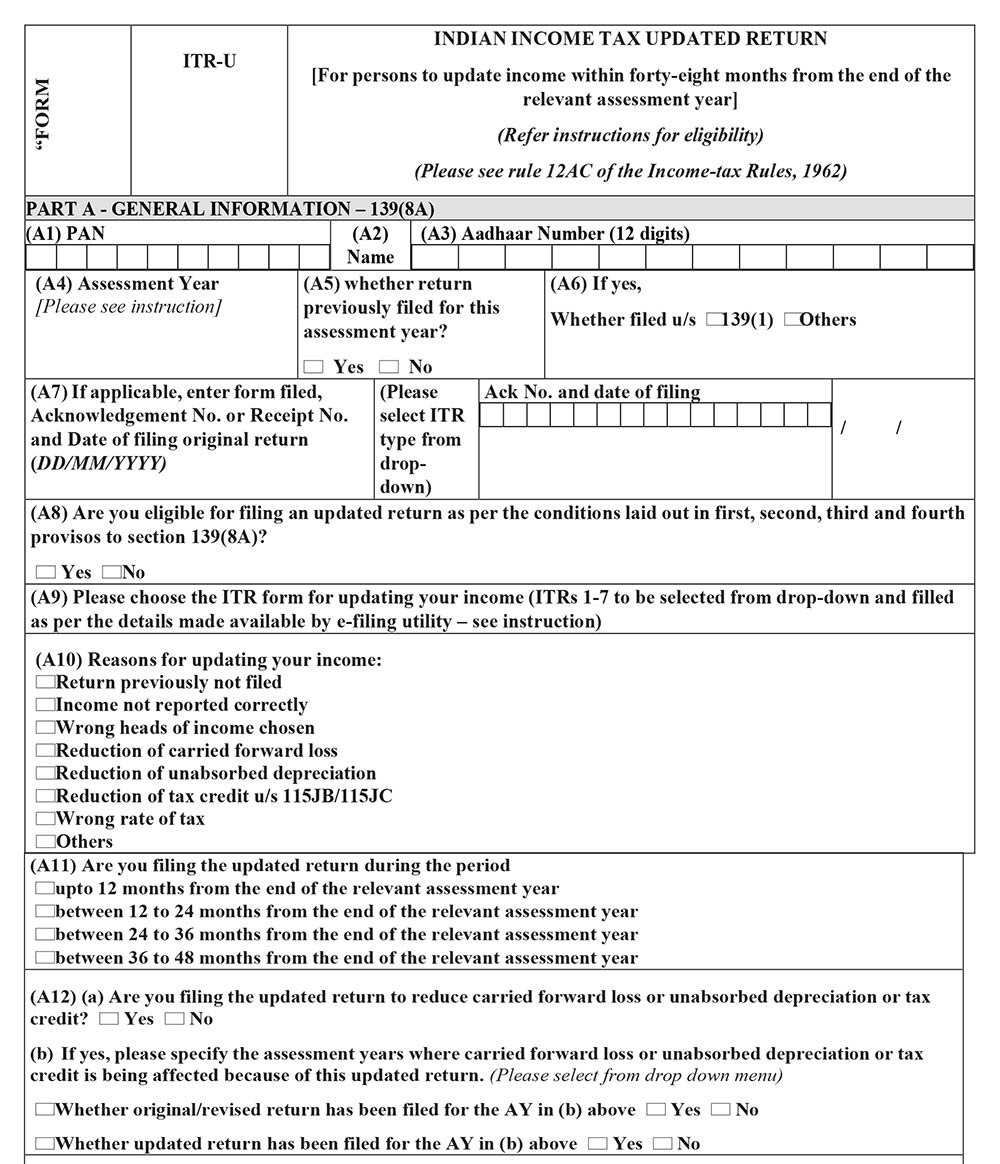

The Updated Income Tax Return, commonly referred to as ITR-U, is a new form introduced by the Indian Income Tax Department. This facility allows you to revise errors or omissions in your income tax returns filed for previous years. It's an opportunity for you to rectify any inaccuracies that could potentially affect your financial records and tax calculations.

What is ITR-U or Updated ITR?

ITR-U is a form that you can file voluntarily while you discover any mistake or omission after your original tax return has been filed. It serves as a declaration of true and correct income, with penalties applying only to additional tax payable, if any.

What is the Purpose of ITR-U?

- The primary purpose of ITR-U is to correct errors in income, deductions, credits, or any other data previously submitted.

- The secondary purpose is to ensure compliance with tax laws and to avoid penalties for non-compliance due to unintentional errors.

Legal Provision

As per the Finance Act 2022, you are allowed to file an updated return within 24 months from the end of the relevant assessment year. This initiative is part of the government’s efforts to enhance voluntary tax compliance and ease the burden of tax litigation.

In the next section, we will delve into who is eligible to file ITR-U and under what circumstances it can be filed.

Eligibility Criteria for Filing ITR-U

Understanding who can file an Updated Income Tax Return and within what timeframe is crucial for compliance and correction of past returns.

Timeframe for Filing

You are permitted to file an ITR-U within 24 months from the end of the assessment year of the original tax return. This allows ample time to identify and rectify any inaccuracies that may have been overlooked by you initially.

Who Can File?

- Any individual or entity that has filed an ITR can opt to file an ITR-U if they discover errors or omissions post-filing.

- It’s applicable to all types of income tax forms except those that are filed in response to a notice from the Income Tax Department.

Types of Corrections Allowed

- Income discrepancies: Misreported or unreported income.

- Deduction and credit errors: Omissions or incorrect claims related to deductions under various sections of the Income Tax Act.

- Personal information updates: Corrections to personal information that does not alter tax calculations.

Step-by-Step Guide to File an Updated ITR (ITR-U)

Filing an ITR-U is a straightforward process, but it requires careful attention to detail to ensure all corrections are accurately reflected. Here’s how you can file an updated return:

Step 1: Log in to the e-Filing portal

Access your account on the Income Tax Department's official e-filing portal.

Step 2: Choose the appropriate form

Select the 'File Updated Return (ITR-U)' option under the e-file section.

Step 3: Fill in the details

Input the relevant year and the details that need to be corrected. Make sure to cross-verify all the new entries with the correct documents.

Step 4: Pay additional tax, if applicable

If the update leads to additional tax payable, ensure that it is paid before submitting the form.

Step 5: Verify and submit

After filling out the form, verify it using your registered mobile number and email. Once verified, submit the form.

Consequences of Not Correcting Mistakes in ITRs

Neglecting errors in your ITR can lead to several adverse effects:

- Penalties and Interest: If discrepancies are discovered during assessments, they may lead to penalties and interest on unpaid taxes.

- Notices from the IT Department: Errors can trigger notices from the Income Tax Department, leading to a scrutiny assessment.

- Impact on Financial Records: Incorrect tax records can impact your financial standing, particularly if you are applying for loans or credit facilities.

Correcting these mistakes proactively using ITR-U is an effective way to avoid such complications.

Common Mistakes and How to Avoid Them

Filing tax returns can be complex, and errors are not uncommon. Here are some of the most frequent mistakes and tips on how to avoid them:

- Incorrect personal details: Double-check your PAN, bank account numbers, and contact information. These errors can delay refunds or cause notices to be issued.

- Misreporting income: Ensure all sources of income, including interest, dividends, and previous employment, are accurately reported. Using a checklist of income sources can help.

- Claiming incorrect deductions: Verify eligibility for deductions under sections like 80C, 80D, etc., before claiming them. Maintain proper documentation to support your claims.

- Not reporting exempt income: While exempt income does not attract tax, it must still be reported. This includes allowances, agricultural income, and certain types of interest.

By being thorough and methodical in gathering documents and filling out your tax return, you can minimise these common errors.

FAQs on ITR-U/Updated ITR

Q1. Can I file an ITR-U if I have already been assessed?

Yes, you can file an ITR-U even after your return has been assessed, provided it is within the 24-month timeframe.

Q2. Is it mandatory to pay a penalty when filing ITR-U?

A penalty may be applicable depending on the nature of the error and the additional tax payable. It is advisable to consult with a tax expert.

Q3. Can I use ITR-U to claim a refund?

No, ITR-U cannot be used to claim a refund. It is intended only to correct inaccuracies that lead to additional tax liability.

Q4. How many times can I file an ITR-U for the same assessment year?

You can file the ITR-U only once for a particular assessment year. Carefully review all changes before submitting.

To Wrap it Up!

Filing an Updated Income Tax Return (ITR-U) is a beneficial provision for taxpayers to amend errors post the original submission deadline. It supports compliance with tax laws and ensures that your financial records reflect accurate information. If you find discrepancies in your past returns, consider using the ITR-U to amend these errors proactively.

If you're unsure about how to proceed with filing an ITR-U or need professional advice, don't hesitate to consult with a tax professional. Remember, accurate tax filing is key to maintaining your financial health and compliance.

Must-Read Articles

How to Calculate Income Tax: A Beginner’s Guide for Salaried Employee

Tax Saving Tips for Freelancers in India in 2024: Maximise Your Savings

How Mutual Fund SIPs Help in Tax Saving?

Old Tax Regime vs New Tax Regime: Which One Should You Opt?

Difference Between Financial Year and Assessment Year

{kind=link}